Swiss safe harbor interest rates

Swiss safe harbor interest rates

Circular Letter Framework 2026

On 29th and 30th January, the Swiss Federal Tax Administration (SFTA) published the latest Circular Letter updating the applicable safe harbor interest rates for intercompany transactions for the fiscal year 2026 (FY26).

Switzerland (lender) to Related Party (borrower)

The minimum interest rate suggested by the SFTA for loans granted by a Swiss entity to its related parties in Swiss francs (CHF) are as follows:

| Type of Loans | 2025 | 2026 | Change |

|---|---|---|---|

| Loans financed with equity | 1.00% | 0.75% | -0.25% |

| Loans financed with debt (up to CHF 10 million) | Third party cost of debt + 0.5% (min. 1.0%) | Third party cost of debt + 0.5% (min. 0.75%) | Similar Spread, min -0.25% |

| Loans financed with debt (exceeding CHF 10 million) | Third party cost of debt + 0.25% (at least 1.0%) | Third party cost of debt + 0.25% (at least 0.75%) | Similar Spread, min -0.25% |

The 2026 minimum rate of 0.75% reflects prevailing market conditions, including lower inflation and Swiss National Bank policy rates observed in late 2025. The spreads over third-party debt costs remain unchanged at 0.5% (up to CHF 10 million) and 0.25% (above CHF 10 million), with an overall minimum of 0.75%.

Switzerland (borrower) from Related Party (lender)

The maximum interest rate suggested by the SFTA for loans granted by a related party to a Swiss entity in CHF should be calculated using the minimum lending rate in CHF increased by a specific spread, as follows:

| Operating loans | Swiss Operating Company | Swiss holding or asset management | Change respect 2025 |

|---|---|---|---|

| CHF 1 million or less | 3.50% (Base Rate ("BR") + spread) (0.75% + 2.75%) |

3.00% (BR + spread) (0.75% + 2.25%) |

This represents a change of - 25 on Basic point ("BP") on the BR and an increase of 25 BP on the spread compared to 2025, which causes no variation on the safe harbor interest rate compared to 2025. |

| Exceeding CHF 1 million | 1.50% (BR + spread) (0.75% + 0.75%) |

1.25% (BR + spread) (0.75% BR + 0.50%) |

This represents a change of - 25 on the BR and no change on the spread compared to 2025, which caused a -0.25 change on the safe harbor interest rate compared to 2025. |

Swiss safe harbor - Foreign currency transactions

Switzerland (lender or borrower) to Related Party (borrower or lender)

The minimum/maximum interest rate suggested by the SFTA for loans granted/received which are equity financed in foreign currency are as follows:

| Country | Currency | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|---|---|---|---|---|

| EU | Euro | 0.75 | 0.75 | 0.50 | 0.25 | 0.50 | 3.00 | 2.50 | 2.50 | 2.50 |

| US | USD | 3.00 | 3.00 | 2.25 | 1.25 | 2.00 | 3.75 | 4.25 | 4.25 | 4.00 |

| AU | AUD | 3.00 | 3.00 | 1.50 | 1.00 | 1.50 | 4.25 | 4.25 | 4.50 | 5.00 |

| BR | BRL | N.A. | 9.50 | 6.00 | 5.75 | 11.25 | 12.75 | 10.25 | 15.50 | 13.50 |

| CA | CAD | 2.75 | 3.25 | 2.50 | 1.50 | 2.50 | 3.75 | 3.50 | 3.25 | 3.25 |

| CN | CNY | 3.50 | 4.25 | 3.75 | 3.75 | 3.75 | 3.00 | 3.00 | 2.00 | 2.25 |

| DN | DKK | 0.75 | 1.00 | 0.75 | 0.50 | 0.50 | 3.25 | 3.00 | 3.00 | 3.25 |

| UK | GBP | 1.75 | 1.75 | 1.50 | 1.00 | 1.25 | 5.25 | 3.75 | 4.50 | 4.00 |

| HK | HKD | 2.25 | 3.25 | 2.50 | 1.50 | 1.50 | 4.25 | 3.00 | 3.50 | 2.50 |

| IN | INR | N.A. | 7.75 | 7.50 | 6.25 | 6.25 | 7.00 | 7.00 | 7.50 | 7.00 |

| IL | ILS | N.A. | 1.25 | N.A. | N.A. | 1.25 | 3.25 | 3.75 | 4.50 | 4.00 |

| JA | JPY | 0.50 | 0.50 | 0.50 | 0.50 | 0.50 | 0.50 | 0.50 | 1.25 | 2.00 |

| PL | PLN | 2.75 | 3.00 | 2.50 | 1.50 | 1.50 | 7.00 | 4.75 | 5.50 | 4.25 |

| SW | SEK | 0.75 | 1.00 | 0.75 | 0.75 | 1.00 | 3.25 | 2.75 | 2.75 | 2.75 |

| SG | SGD | 2.25 | 2.75 | 2.25 | 1.25 | 1.50 | 4.00 | 3.00 | 3.25 | 2.25 |

| ZA | ZAR | 7.50 | 8.50 | 7.75 | 5.75 | 6.50 | 8.75 | 8.25 | 8.25 | 7.00 |

| AE | AED | 3.25 | 3.25 | 2.75 | 2.00 | 2.50 | 4.00 | 4.25 | 5.00 | 4.25 |

Switzerland (lender) to Related Party (borrower)

Minimum interest rates for loan receivables:

- Foreign currency loans: If the foreign currency rate is below the CHF safe harbor rate, the CHF rate must be applied.

- Equity-financed: Safe harbor rates apply.

- External debt-financed: Third-party borrowing costs (including fees) plus a 0.5% markup, but in any case, not below the safe harbor rates.

Switzerland (borrower) from Related Party (lender)

Maximum interest rates for loan payables under the Swiss safe harbor rules:

- Foreign currency loans (safe harbor): CHF base + spread

- Up to CHF 1M equivalent: 2.75% / 2.25%

- Above CHF 1M equivalent: 0.75% / 0.50%.

Financial markets

Arm's length interest rates

Financial markets are very volatile and sensitive to external shocks; market interest rates change very quickly and often. In the current economic environment, the markets have experienced a significant reduction in interest rates, driven by the monetary policy of major central banks to reduce interest rates, considering that inflation is not a significant problem in the short-term horizon.

However, due to several variables (e.g., escalating US customs tariffs under President Trump, increased European defense spending amid NATO's military budget hike, high volatility in precious metals, key national and state elections in Europe (e.g., Danish parliamentary vote, German regional contests, Portuguese presidential), and the deepening real estate crisis in China, among others), we foresee significant volatility in the markets in 2026.

In addition, it is important to highlight that Swiss safe harbor rates do not necessarily reflect arm’s length interest rates. Therefore, even if they are accepted in Switzerland, they may still be challenged by foreign tax authorities.

In a Federal Supreme Court decision (9C_690/2022, 17 July 2024), the Court clarified that when a taxpayer deviates from the safe harbor interest rates, it effectively waives their application. Therefore, in the event of a tax audit, tax authorities are no longer bound by the safe harbor rates and may determine arm’s length interest rates based on market conditions. Such adjustments may result in interest rates that differ significantly from the safe harbor rates.

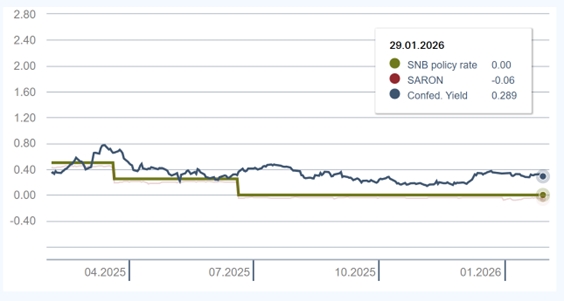

Swiss Confederation bonds yield curve

The graph below shows evidence of the disinflationary environment. The SNB’s decision to move to and maintain a 0.00% policy rate from mid-2025 coupled with the compression of long-term bond yields—reflects a decisive monetary response to the cooling price pressures seen over the past year.

Source: SNB - Current Interest Rates and exchange rates

Conclusions

Transfer pricing key takeaway

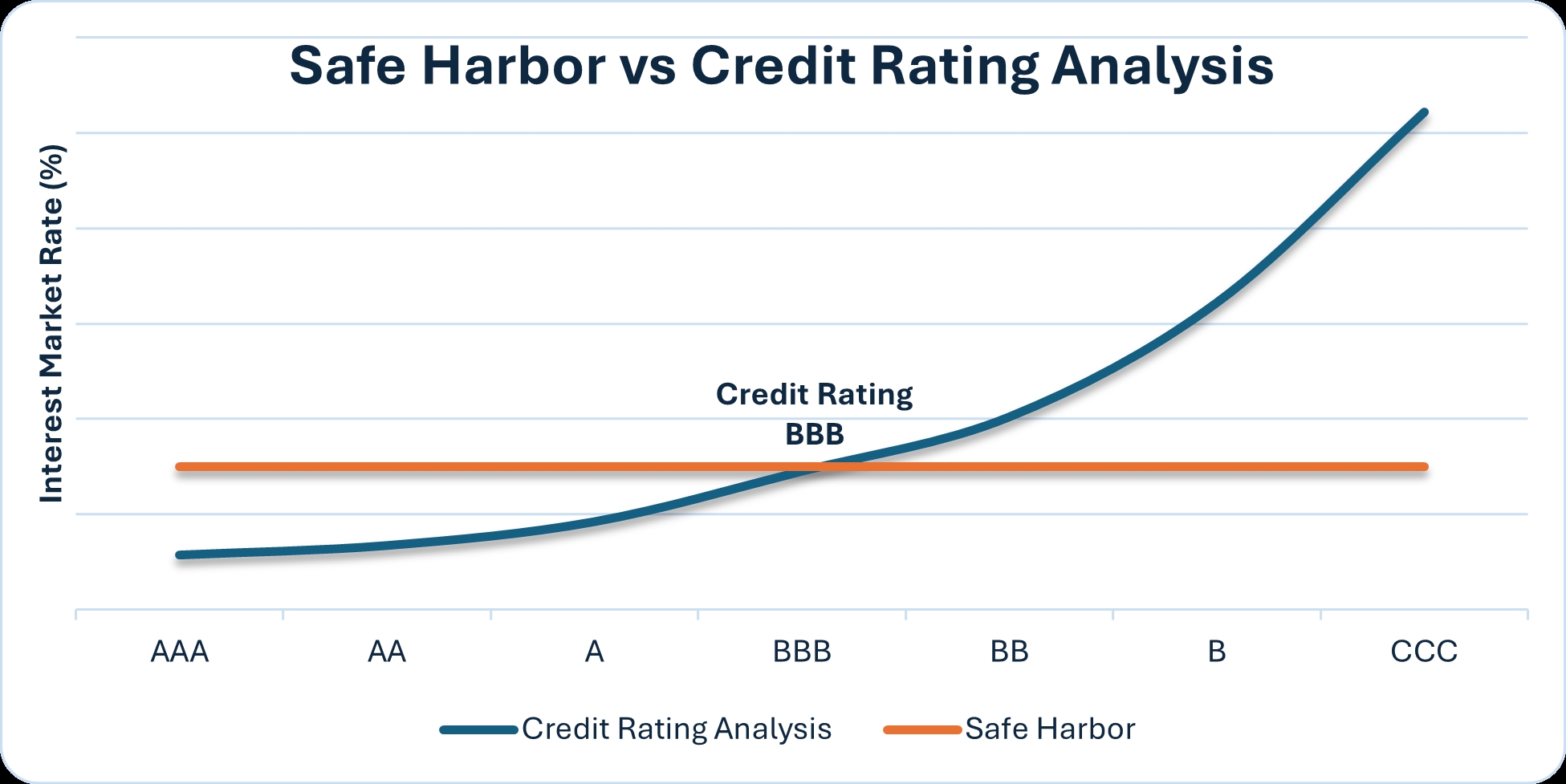

Swiss Safe Harbor rates are easy to apply but do not reflect a company’s real credit risk. For companies with a credit rating ("CR") better than BBB, Swiss Safe Harbor interest rates are usually higher than arm´s length rates, creating a risk for the company, since a third party would have lent at a lower rate. This situation will put the company in a potential tax risk locally since the Swiss harbor interest rare would be higher than an arm´s length interest rate.

Transfer pricing opportunities

The Swiss tax authorities will accept a deviation from the Swiss safe harbor rates if the taxpayer can demonstrate that the interest rate applied is an arm's length interest rate based on the following:

- Borrower's CR

- Benchmark analysis based on the CR and the loan terms and conditions

Higher interest rates supported by a transfer pricing analysis allow Swiss entities to charge more interest to their related parties, and if the related party is located in a jurisdiction with a higher tax rate than Switzerland, it will generate tax savings for the Group.